0x2c33...0563Profit

+$6.6M

Volume

$738.7M

Substantial-Service's 50-0 Polymarket Run Hides a $15K Graveyard

The Perfect Record That Isn't

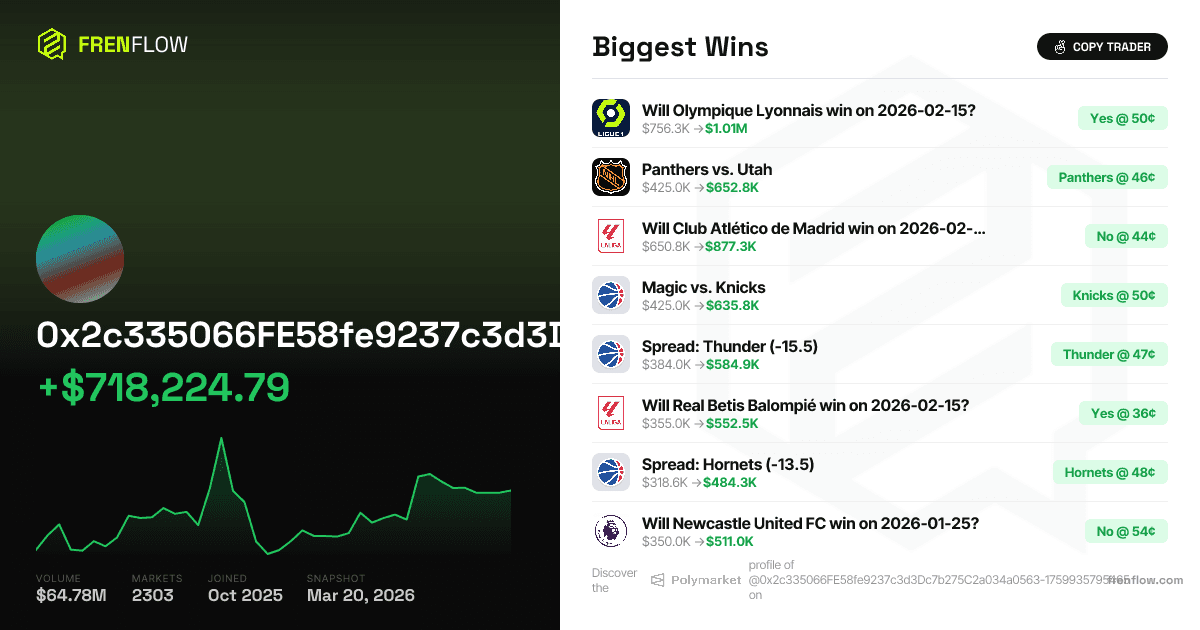

Fifty closed positions, fifty wins, $5.57 million in profit, and an average entry price of 47 cents. The trader known as Substantial-Service has pushed $64.78 million in volume through Polymarket since October 2025—five months of relentless sports betting across NBA spreads, La Liga match outcomes, NCAA over/unders, and NHL moneylines. The headline stat is a 50-0 closed record. The thesis of this article is that the record is an artifact of position management, not prophetic skill, and that the trader's actual edge—while real—is far more modest and far more fragile than the top-line numbers suggest.

Look past the closed trades and into the open positions. Fifteen are currently sitting on the books. Fourteen of them are losers, most resolved to zero. Combined unrealized losses: roughly $15,000. That's a rounding error against $5.57M in winnings, but it reveals the mechanism: Substantial-Service doesn't close losing trades. They let them expire worthless, keeping them off the "closed" ledger entirely. The 50-0 record is real in the narrowest technical sense and meaningless as a measure of predictive accuracy.

Anatomy of the Sizing Strategy

The real story is in how this trader allocates capital. The top 25 winning trades range from $181K to $756K in share purchases, with a median around $275K. Average entry price across winners: 47 cents. Average ROI on those wins: approximately 105%. This is a trader buying near-coin-flip outcomes and collecting the full payout when they hit.

| Trade | Entry Price | Shares Bought | Profit | ROI | Pattern |

|---|---|---|---|---|---|

| Olympique Lyonnais win | 49.9¢ | $756K | $251K | 66.4% | Near-even money, massive size |

| Panthers vs. Utah | 46.4¢ | $425K | $228K | 115.5% | Slight underdog, large size |

| Atlético Madrid "No" win (Feb 14) | 43.6¢ | $651K | $227K | 79.8% | Fading the favorite, huge size |

| Real Betis win (Feb 15) | 36.5¢ | $355K | $197K | 152.4% | Longest odds in top trades |

| Nottingham Forest "No" win (Feb 26) | 36.2¢ | $226K | $144K | 176.0% | Fading favorite, smaller size |

Two patterns emerge immediately. First, the position sizing scales with the entry price—when the odds are closer to even (49–57¢), the trader goes bigger ($400K–$756K). When buying at 36–43¢, the positions shrink to $200K–$355K. This is crude but rational bankroll management: larger bets on higher-probability outcomes, smaller bets on longshots. Second, the sport and league don't seem to matter. NBA, La Liga, Ligue 1, NHL, college basketball, esports—Substantial-Service bets across all of them. This is not someone with deep domain expertise in one sport. This is someone exploiting a structural feature of the market itself.

The Edge: Liquidity Exploitation at Scale

Here's what I think is actually happening. Polymarket sports markets, especially the less liquid ones—A-League over/unders, La Liga match results for mid-table clubs, college basketball spreads for teams like Loyola Marymount—often have wide bid-ask spreads and stale pricing relative to what a sharp bettor can find on centralized sportsbooks. The edge isn't predicting outcomes. The edge is arbitrage or near-arbitrage against sharper lines elsewhere.

Consider the Olympique Lyonnais trade. The trader bought $756K in "Yes" shares at 49.9 cents. Lyon were sitting 10th in Ligue 1 at the start of February with only one domestic win in 2026 at that point—though their form may have shifted by the time of the match. Buying "Yes" at even money for a side in that kind of form is a head-scratcher on the surface. It's only rational if the Polymarket price was meaningfully mispriced relative to true probability—whether because of stale liquidity on Polymarket, a favorable matchup against a weaker opponent, or sharper centralized sportsbook lines offering Lyon at slightly higher implied probability. We don't have the specific sportsbook line to confirm the gap, but the trade's profitability suggests some form of market inefficiency was being exploited. That kind of edge, applied to $756K in shares, is how you generate the $251K profit we see.

The same logic explains the Atlético Madrid "No" trade at 43.6 cents. Betting that Atlético wouldn't win implies you believed their win probability was below 56.4%. For a top La Liga side, that's plausible in many match contexts—draws happen frequently in Spanish football. If a sportsbook had the draw + opponent win probability at 60%, Polymarket's 56.4% implied was a buy.

The total volume of $64.78M against $718K in reported profit gives a razor-thin 1.11% margin. That's consistent with arbitrage or soft-line exploitation rather than high-conviction directional betting. Nobody putting up $200K–$756K per trade on genuine prediction would tolerate a 1.11% margin. You'd need to be very confident in your edge and very confident in your ability to size correctly.

The Graveyard of Open Positions

The open positions tell us something the closed record obscures: the strategy fails regularly, just at smaller sizes.

| Open Position | Entry | Current | Shares | Unrealized Loss |

|---|---|---|---|---|

| Seahawks spread (Rams) | 56.0¢ | 0.0¢ | $274 | -$153 |

| Gabriel Diallo vs. Shelton | 15.8¢ | 0.0¢ | $1K | -$160 |

| CD Castellón win | 50.0¢ | 0.0¢ | $829 | -$415 |

| Cavaliers spread (Magic) | 45.0¢ | 0.0¢ | $2K | -$688 |

| Real Madrid La Liga | 58.5¢ | 17.0¢ | $2K | -$835 |

| Xtreme Gaming (Dota 2) | 62.9¢ | 0.0¢ | $3K | -$2K |

| Memphis vs. Wichita State O/U | 52.0¢ | 0.0¢ | $5K | -$2K |

Notice the pattern: every losing position is sized between $274 and $9K. The biggest open loser—the Rams-Seahawks over/under at $9K—is still two orders of magnitude smaller than the largest winner. This isn't coincidence. The trader appears to probe markets with small positions, then scale up dramatically when conditions are right. The probe bets that fail stay small and stay "open" even after resolution, creating the illusion of a spotless record.

The one genuinely large open position is the Georgia Bulldogs spread: $118K in shares at 47 cents, now trading at $1.00. That's $62K in unrealized profit—another winner that, when closed, will extend the streak to 51-0.

The Real Madrid La Liga futures position is the most interesting outlier. Bought at 58.5 cents, now at 17 cents, with a $2K position. This is the only open trade that looks like a genuine medium-term prediction rather than a single-game arbitrage play. It's also losing badly—Real Madrid's La Liga odds have cratered, which makes sense if the trader's edge is in short-duration sports markets, not in season-long futures.

What $718K in Profit Actually Means

The reported total profit of $718K against the $5.57M in closed-position winnings creates an apparent contradiction. If 50 closed trades generated $5.57M in profit and the total profit is only $718K, there are substantial losses not captured in the closed positions—or the $64.78M in volume includes round-trip costs, slippage, and positions that were entered and exited at losses before the current snapshot.

The most likely explanation: Substantial-Service runs a much larger book than what appears in the top-25 list. With 2,303 markets traded, we're only seeing the top performers. The remaining ~2,250 markets include the small probes, the failed arbitrage attempts, and the positions that were closed at small losses or scratched at breakeven. At 1.11% overall margin on $64.78M in volume, the all-in profit is $718K—solid, but not the fantasy that a 50-0 record implies.

The Kelly criterion offers a useful sanity check. If the trader's true win rate across all positions (not just the big ones that hit) is, say, 55% with an average payoff of 2:1, the optimal Kelly fraction would be around 7.5% of bankroll per bet. The actual sizing on winners—$200K to $756K—implies a working bankroll of $2.7M to $10M, consistent with a well-capitalized operation that can tolerate the variance inherent in sports market arbitrage.

The Real Question: Is This Sustainable?

Five months, $64.78M in volume, $718K in profit. That's a $1.7M annualized run rate at current pace. The risk is straightforward: this strategy depends on Polymarket sports markets remaining inefficient relative to centralized sportsbooks. As volume grows and more sophisticated participants enter, the bid-ask spreads tighten and the arbitrage windows close.

There's a second risk buried in the position sizing. The largest single trade was $756K in shares on a Ligue 1 match. If that bet had lost, it would have wiped out more than the total reported profit. The trader has been running a strategy where a single large loss could erase months of accumulated edge. So far, the large bets have all landed. The small probes have absorbed the losses. But the Kelly math doesn't care about track records—it cares about expected value per unit of risk, and concentrating $756K on a single football match at 49.9 cents is, by any measure, aggressive.

Substantial-Service's current balance of $118K suggests the profits have been withdrawn or redeployed elsewhere. The account isn't sitting on a war chest. If the Polymarket sports ecosystem continues to grow—and the FrenFlow trader profile shows zero profile views despite $64.78M in volume, meaning this operation has flown entirely under the radar—then Substantial-Service's window of edge may already be narrowing.

The 50-0 record is a parlor trick. The $718K in profit is real. The question is whether the strategy that produced it can survive the attention.

Frequently Asked Questions

How much has Substantial-Service made on Polymarket?

Substantial-Service has generated $718K in total profit on $64.78M in trading volume since joining Polymarket in October 2025. The trader's closed positions show $5.57M in profit across 50 winning trades with zero closed losses, but this figure does not account for smaller losing positions that remain open or were absorbed elsewhere in the $64.78M volume.

What sports does Substantial-Service bet on?

The trader bets across a wide range of sports and leagues: NBA, NFL, NHL, La Liga, Ligue 1, MLS, A-League, college basketball, and even esports (Dota 2, Counter-Strike). This breadth suggests a cross-market arbitrage strategy rather than deep expertise in any single sport.

Is a 50-0 win record on Polymarket legitimate?

Technically, Substantial-Service's 50 closed positions are all winners. However, the trader has 15 open positions, 14 of which are losing or have resolved to zero. The losses are kept in "open" status rather than closed, which inflates the win record. The actual win rate across all positions is substantially lower than 100%.

What is Substantial-Service's Polymarket trading strategy?

The data suggests a liquidity exploitation strategy: the trader identifies sports markets on Polymarket where the implied probability diverges from centralized sportsbook lines, enters large positions at favorable prices (average entry ~47 cents), and collects the payout when the market resolves. Small "probe" bets of $274–$9K test market conditions before the trader scales up to $200K–$756K on high-conviction plays.

How much does Substantial-Service risk per trade on Polymarket?

The trader's largest single position was $756K in shares on an Olympique Lyonnais match. Winning positions typically range from $200K to $650K, while losing positions are kept to $274–$9K. This asymmetric sizing is key to the strategy: wins are large and losses are small, creating the appearance of a perfect record while maintaining a 1.11% overall profit margin.

Related articles

blindStaking's $710K Week on Polymarket: Sports Betting at Scale

Mar 22, 2026

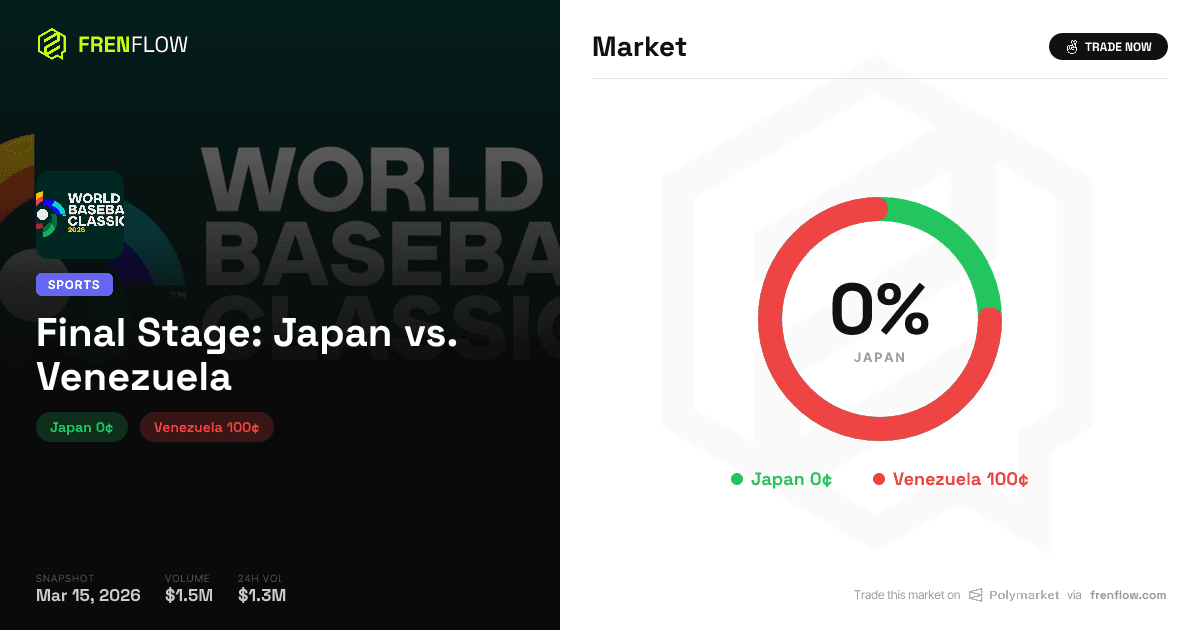

Japan vs Venezuela WBC: Polymarket Prices an 88% Rout

Mar 15, 2026

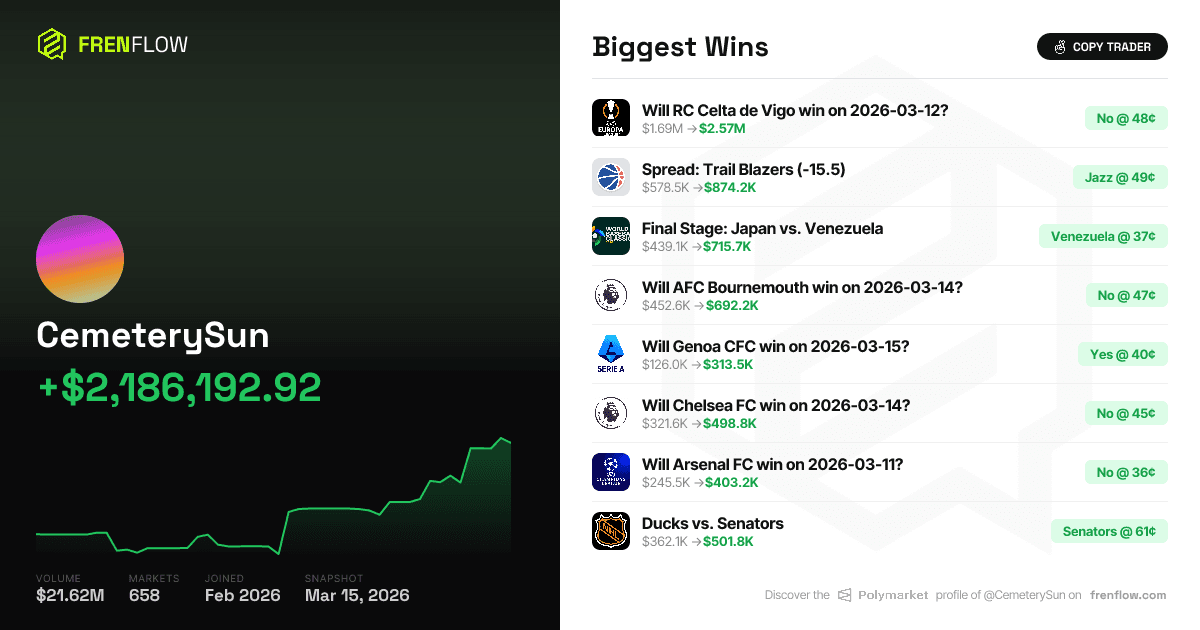

CemeterySun: 50-0 on Polymarket with $3.37M in Closed Wins

Mar 15, 2026