Finland Dominates Eurovision 2026 Odds on Polymarket

The Market Has a Favorite, but the Math Is Stranger Than It Looks

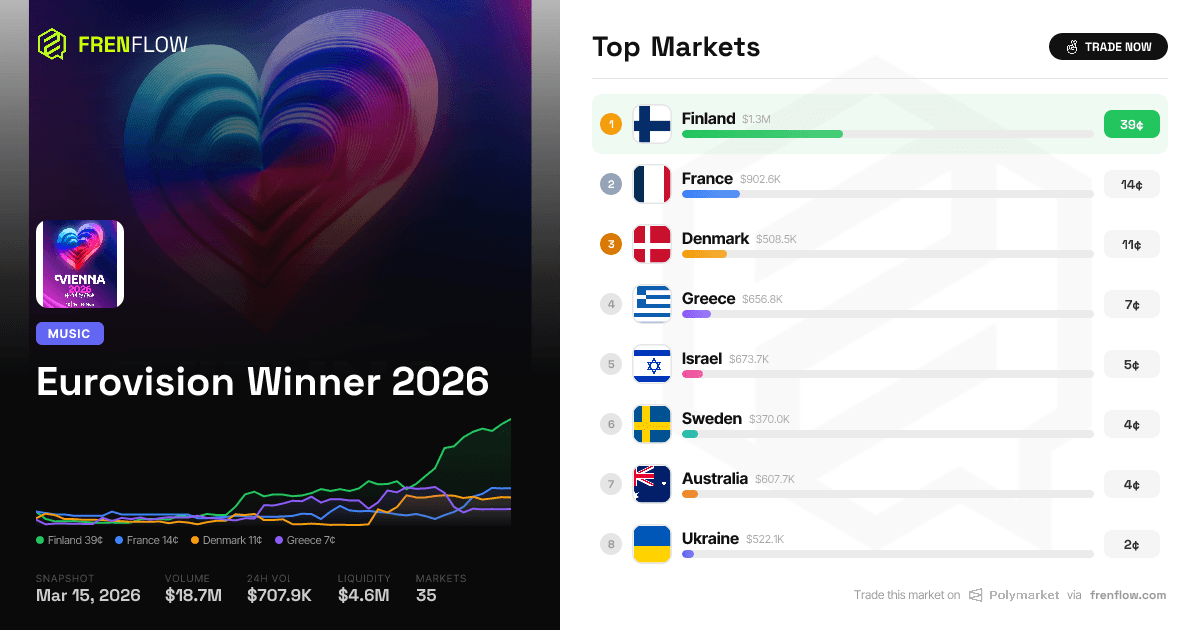

Finland trades at 39.3 cents on $1.30M in volume—the fattest position in the Eurovision 2026 market—yet the combined implied probabilities of all listed outcomes sum to approximately 102%, reflecting a relatively tight vig for a 35-outcome contest two months from resolution. That leaves a genuine multi-outcome market where Finland alone holds nearly as much implied probability as France, Denmark, Greece, and Israel combined. The question isn't whether Finland is the favorite. It's whether 39 cents is cheap or expensive for a Eurovision frontrunner with two months of national-selection chaos still unfolding across Europe.

The Eurovision Song Contest 2026—the 70th edition—runs semi-finals on May 12 and 14, with the grand final on May 16 at Vienna's Wiener Stadthalle. That's exactly 62 days from today. National selections are still wrapping up: Sweden just crowned Felicia with "My System" at Melodifestivalen, Poland selected Alicja with "Pray," and Romania chose Alexandra Căpitănescu's "Choke Me" at Selecția Națională. Multiple countries haven't finalized entries. The market is pricing a race where some horses haven't even been saddled.

Finland: Frontrunner Economics

At 39.3 cents, a $1,000 Yes bet on Finland returns $2,545 if correct—a 2.54x payout over roughly two months. That's attractive, but only if the true probability exceeds ~40%. The question: does the betting market's wisdom align with the broader Eurovision prediction ecosystem?

The answer appears to be yes. Multiple Eurovision odds aggregators and YouTube prediction channels have placed Finland at or near the top of their rankings throughout March 2026. Finland's $1.30M in volume is the highest of any single outcome, and the 39.3-cent price represents genuine conviction rather than a thin book propped up by one whale. For context, the market's total liquidity sits at $4.54M—meaning Finland's price is backstopped by a relatively deep order book. Moving Finland's price by a full cent would require meaningful capital, not a stray retail bet.

But Eurovision frontrunners have a complicated history with winning. Early favorites frequently fade. In 2024, Croatia's Baby Lasagna led betting markets for weeks before finishing second to Switzerland's Nemo. The lesson: a 39-cent price two months out carries real risk of mean-reversion, especially as rehearsal footage and semi-final draws shift sentiment.

| Country | Price | Volume | Implied Prob. | Signal |

|---|---|---|---|---|

| Finland | 39.3¢ | $1.30M | 39.3% | Clear frontrunner; deepest volume confirms broad conviction |

| France | 14.4¢ | $903K | 14.4% | Strong second with outsized volume—smart money lane? |

| Denmark | 11.1¢ | $508K | 11.1% | Surging; new entrant to top 3 per odds trackers |

| Greece | 7.0¢ | $657K | 7.0% | Volume/price ratio suggests active trading, not just holding |

| Israel | 4.6¢ | $674K | 4.6% | Disproportionate volume driven by geopolitical news flow |

| Australia | 3.9¢ | $608K | 3.9% | Steady but unremarkable; typical mid-tier Eurovision contender |

| Sweden | 3.8¢ | $370K | 3.8% | Melodifestivalen just concluded; price may lag new information |

The France–Denmark Squeeze

The more analytically interesting positions sit at 14.4 cents (France) and 11.1 cents (Denmark). France carries $903K in volume—the second-highest in the market—at a price that implies roughly a 1-in-7 chance. A $1,000 Yes position on France pays $6,944 if correct. That's a 6.94x return in two months. If you believe France's true probability is above 15%, the expected value is positive.

Denmark's surge is the market's freshest signal. At 11.1 cents on $508K volume, Denmark has climbed into the top three, confirmed by multiple Eurovision odds trackers updating as recently as five days ago. The combination of rising price and moderate-but-growing volume suggests this isn't a pump—it's accumulation. Someone (or many someones) are building a Denmark position before the semi-final draw locks in the competitive landscape.

The gap between Finland (39.3¢) and France (14.4¢) is 24.9 cents—a massive spread for a contest where the winner is determined by a single night's voting. In a typical Eurovision, the pre-contest favorite wins roughly 25-30% of the time across the past decade. If that base rate holds, Finland at 39.3¢ is overpriced relative to the historical win rate of frontrunners, and the second and third favorites are likely underpriced.

This creates a structural trade: sell Finland, buy France and Denmark in a ratio that captures the spread. The risk is that Finland's entry is genuinely generational—a "Euphoria" or "Arcade"-level lock—but even those entries didn't trade at 39% implied probability this far out.

The Boycott Shadow and Israel's Unusual Volume

The web research confirms what the market already suspects: Eurovision 2026 faces what multiple media outlets have described as one of the largest boycotts in contest history, over the decision to permit Israel's participation. Switzerland's 2024 winner Nemo returned their trophy to the EBU in protest, and Charlie McGettigan, who won for Ireland in 1994 alongside Paul Harrington, stated that he would return their trophy as well—an unprecedented show of opposition from past winners spanning three decades. Multiple countries' broadcasters confirmed boycotts.

Israel trades at 4.6 cents—a modest implied probability—but carries $674K in volume, more than Sweden ($370K), Denmark ($508K), or any country priced below 5 cents except San Marino's curious $549K (at just 0.1 cents, suggesting heavy No-side trading). Israel's volume-to-price ratio is the most distorted in the market. At 4.6 cents, $674K in volume suggests enormous churn: traders entering and exiting positions as geopolitical news shifts. This is event-driven volatility, not conviction.

The boycott also matters structurally. Fewer competing countries could theoretically concentrate votes among remaining participants, boosting the probability for favorites like Finland and France. However, the countries boycotting tend to be Eurovision's cultural powerhouses (details depend on which broadcasters finalize their withdrawal), so the competitive field may be weaker in some respects but also less predictable.

Liquidity Traps in the Long Tail

Twenty countries trade at 0.5 cents or below. Together, they represent roughly 7% of implied probability and over $8M in cumulative volume. This is where the market's structure gets deceptive.

Consider San Marino: 0.1 cents, $549K volume. Nobody is buying San Marino to win Eurovision. That volume represents No-side traders collecting fractional returns on outcomes they view as nearly impossible, plus a smattering of lottery-ticket Yes bets. The house edge for No sellers is thin—you tie up capital for two months to earn 0.1% on resolution—but in aggregate, these micro-positions generate substantial market activity that inflates the total volume figure.

The real money—the capital with genuine predictive intent—concentrates in the top seven or eight outcomes. Roughly $5.7M in volume sits behind countries priced above 2 cents. That's the "real" Eurovision prediction market. The remaining ~$13M is a combination of No-side harvesting, meme bets, and position cycling across dozens of low-probability outcomes.

Trackers on FrenFlow allow you to monitor how these positions shift as national selections finalize and rehearsal buzz builds in April.

What Moves This Market Next

Three catalysts sit between now and the May 16 final:

Late national selections (March–April): Several countries haven't finalized entries. Each announcement can move prices 2-5 cents if the selected artist has a strong fan base or a song that generates immediate viral momentum. Sweden's Felicia was just selected; watch for market reaction over the next week as "My System" circulates.

Running order reveal: The semi-final allocation draw already took place on January 12, 2026, but the precise running order within each semi-final—which significantly affects outcomes—has yet to be announced. A strong favorite buried early in the running order faces a viewer-memory disadvantage; a mid-tier entry in a favorable late slot can ride momentum into the final. This remains an underpriced catalyst.

Rehearsal footage (early May): When artists arrive in Vienna and rehearsal clips leak, the market reprices violently. In past years, frontrunners have gained or lost 10+ cents in a single day based on staging reveals. Finland's 39.3 cents is vulnerable to any rehearsal footage that disappoints relative to sky-high expectations.

| Catalyst | Expected Timing | Potential Impact | Favors |

|---|---|---|---|

| Remaining national selections | Now through April | 2-5¢ per entry | Mid-tier contenders with strong songs |

| Semi-final allocation draw | Late March / April | 3-8¢ for semi-final-bound entries | Auto-qualifiers (host + Big 4) unaffected |

| Rehearsal footage in Vienna | May 5-11 | 5-15¢ for top contenders | Entries with strong staging concepts |

| Semi-final results | May 12, 14 | Binary for non-auto-qualifier | Finland (if in semi) faces elimination gate |

Note: France, as a Big Four member, bypasses semi-finals entirely—a structural advantage the market may be underpricing at 14.4 cents.

The Verdict: Finland Is Overvalued, France Is the Smarter Bet

The market's confidence level in Finland—39.3%—exceeds the historical base rate for Eurovision frontrunners at this stage by roughly 10-15 percentage points. That doesn't mean Finland won't win. It means the price already embeds a premium for the hype, and rational capital should be exploring the second and third tier.

France at 14.4 cents offers asymmetric upside: a Big Four auto-qualifier (no semi-final risk), $903K in volume suggesting institutional-grade conviction, and a price that implies roughly 1-in-7 odds in a contest where the second favorite historically wins about 15% of the time. Denmark at 11.1 cents is the momentum play, though its thinner volume suggests the move could reverse quickly.

The disciplined trade: underweight Finland, overweight France, and hold a small Denmark position as a momentum kicker. The reckless trade: buy Greece at 7 cents and pray for a Zorba-era televote surge. The smart observation: with 62 days until the final, this market will reprice at least twice more before anyone sings a note in Vienna.

Frequently Asked Questions

Who is the favorite to win Eurovision 2026 on Polymarket?

As of March 15, 2026, Finland leads the Polymarket Eurovision 2026 market at 39.3 cents (39.3% implied probability), followed by France at 14.4 cents and Denmark at 11.1 cents. Finland has attracted the most volume of any single outcome at $1.30M.

When is Eurovision 2026 and where is it held?

Eurovision 2026 takes place at the Wiener Stadthalle in Vienna, Austria. The semi-finals are scheduled for May 12 and May 14, with the grand final on May 16, 2026.

How much money has been bet on Eurovision 2026 on Polymarket?

The Eurovision 2026 market on Polymarket has generated $18.73M in total volume across all outcomes, with $4.54M in current liquidity. However, roughly $13M of that volume is concentrated in long-tail outcomes priced below 2 cents, much of it driven by No-side trading rather than predictive conviction.

Which countries are boycotting Eurovision 2026?

Multiple countries have announced boycotts of Eurovision 2026 over the EBU's decision to permit Israel's participation. Switzerland's 2024 winner Nemo returned their trophy to the EBU in protest, and Ireland's 1994 winner Charlie McGettigan stated he would return his trophy as well. The boycott has been widely described by media outlets as among the largest in Eurovision history, though the full list of boycotting broadcasters continues to evolve.

Is France a good bet for Eurovision 2026?

France trades at 14.4 cents on Polymarket, implying roughly a 1-in-7 chance of winning. As a Big Four member, France automatically qualifies for the grand final, bypassing semi-final elimination risk. With $903K in volume—the second-highest in the market—France represents the deepest liquidity among non-frontrunner contenders and offers a 6.94x payout if correct.