Crude Oil Above $120? Polymarket Bets $29M on a March Spike

The $200 Strike Is the Tell

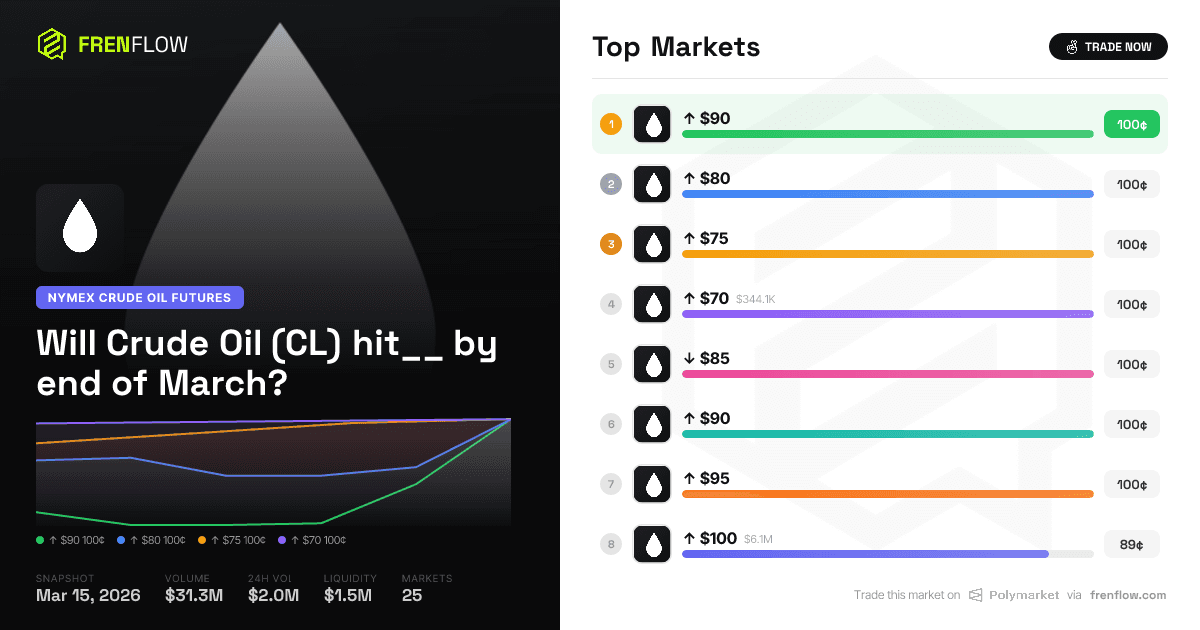

Forget the $120 contract trading at 50.5 cents. The most revealing price in this $29.4 million crude oil market is the $200 strike — a contract implying a near-doubling from roughly current levels — which has attracted $4.67 million in volume despite trading at just 3.9 cents. That's more volume than the $140 and $130 strikes combined. Someone, or many someones, is spending real money on a scenario that would require the largest single-month oil price surge since the 1973 embargo. Either the deep out-of-the-money crowd knows something the front of the curve doesn't, or this is the most expensive lottery ticket on Polymarket.

The answer matters because the entire strip — 25 individual strike contracts resolving against CME front-month settlement prices by March 31 — paints a portrait of a market that has already repriced a massive supply shock into the near term. With only 17 calendar days remaining (and roughly 12 CME trading sessions), the implied probability distribution suggests traders see crude oil centered around $110-$120 with fat right tails extending well past $150. That isn't a normal oil market. That's a crisis market.

Decoding the Probability Curve

The best way to read this strip is as a cumulative distribution function — each "hit" contract tells you the market's implied probability that oil reaches at least that level by expiration.

| Strike | Implied Prob. | Volume | Signal |

|---|---|---|---|

| ↑ $90 | 100.0% | $0 | Already resolved or priced as certain — oil is above $90 now |

| ↑ $95 | 100.0% | $0 | Same — no remaining uncertainty |

| ↑ $100 | 90.5% | $5.87M | Near-certainty, but $5.87M in volume says some traders questioned it |

| ↑ $105 | 84.7% | $1.78M | ~85% chance of $105 — roughly where the current front-month likely trades |

| ↑ $110 | 73.5% | $3.01M | Three-in-four odds of a $110 print |

| ↑ $120 | 50.5% | $3.04M | Coin flip — the market's effective median |

| ↑ $130 | 31.5% | $1.21M | One-in-three for $130 |

| ↑ $140 | 23.0% | $941K | Nearly one-in-four |

| ↑ $150 | 16.4% | $4.35M | One-in-six, but massive volume |

| ↑ $180 | 5.9% | $1.89M | Long-shot, yet almost $2M traded |

| ↑ $200 | 3.9% | $4.67M | Highest single-strike volume in the strip |

Two things jump out immediately. First, the $90 and $95 strikes have resolved at 100 cents with zero volume, confirming that crude oil's CME settlement price has already printed above $95 — likely well above, given the $100 strike sits at 90.5%. The market is telling us the front-month contract is trading somewhere in the $105-$110 range right now, with the $105 strike at 84.7% and the $110 at 73.5%.

Second, the volume distribution is inverted from what you'd expect in a normal commodity market. In a calm environment, the at-the-money strikes should dominate volume. Here, the $200 strike ($4.67M) has generated more volume than the $120 strike ($3.04M), which is the market's median outcome. The $150 strike, at 16.4 cents, has drawn $4.35M — roughly the same volume as the $100 strike at 90.5 cents. Volume is concentrating in the tails, not the body.

What the Tail Volume Is Pricing

When traders pour $4.67M into a 3.9-cent contract, the math is straightforward. A $1,000 position at 3.9 cents returns $25,641 if crude oil settles at or above $200 on any CME trading day through March 31 — a 25.6x payout. At $4.67M in volume, the market has processed approximately $182,000 in potential payouts at these odds (assuming a mix of buys and sells). But the sheer churn suggests active two-way trading: some participants are selling this contract as a premium-harvesting strategy, while others are buying it as tail-risk insurance or a speculative lottery.

The $150 strike is where the analysis gets more disciplined. At 16.4 cents, a buyer is paying $164 per contract to win $1,000 — a 6.1x return, or roughly a 510% gain in under three weeks. For this to be a positive expected-value trade, the buyer needs to believe the true probability of $150 oil by month-end exceeds 16.4%. That's not impossible in a genuine supply disruption — oil rose from $97 to $147 between February and July 2008 — but compressing that move into 17 days requires an extraordinary catalyst.

The downside strip is instructive by contrast. The ↓$75 contract (oil falling below $75) trades at 10.5 cents, and the ↓$80 at 17.5 cents. Combined, they imply about a one-in-six chance of a collapse back below $80. That's notable — it means the market sees the risk distribution as dramatically asymmetric. Upside tail risk is being priced at roughly 3-5x the density of equivalent downside tails.

Liquidity: The Thin Ice Beneath the Price

The headline numbers — $29.4M total volume, $2.39M in the last 24 hours — suggest a liquid, well-traded market. Dig deeper and the picture shifts. Total liquidity across all 25 strikes stands at just $1.51M. That's a volume-to-liquidity ratio of roughly 19:1, meaning for every dollar sitting in order books, $19 has already traded through.

What does that imply? This market is momentum-prone. A single trader deploying $200K could meaningfully move prices across multiple strikes, especially on the thinner tails where the $180 and $200 contracts may have only tens of thousands in resting liquidity. The 24-hour volume of $2.39M represents 158% of total current liquidity — the entire book could theoretically turn over more than once per day.

For traders: these are not prices you can hit at size. The 50.5 cents on the $120 strike is an indicative midpoint, not an executable level for a six-figure position. Anyone looking to express a view here needs to work orders patiently or accept significant slippage. The prices are more useful as probability signals than as tradeable levels.

The 12-Session Countdown

March 31 is a Tuesday. Assuming standard CME holidays and weekend closures, roughly 12 trading sessions remain from today (March 14, a Saturday — so beginning Monday, March 16). That's 12 settlement prints for oil to hit any given strike.

The resolution mechanism matters: only the official CME daily settlement price counts. Not the intraday high. Not the Globex overnight spike. The settlement price, which CME calculates using a weighted average during a defined closing window. Oil can trade $130 intraday and settle at $124 — the $130 strike wouldn't trigger.

This makes the upside strikes slightly harder to hit than a naive reading suggests. In the 2022 Russia-Ukraine spike, WTI crude touched $130.50 intraday on March 7 but settled at $119.40. The $120 strike on this Polymarket contract would have just barely missed resolution that day. Settlement methodology acts as a dampener on extreme prints, which means the true probability of hitting round-number strikes may be 5-10 percentage points lower than what intraday price action would suggest.

Catalysts That Could Move Oil $20+ by March 31

The market's pricing implies at least a coin-flip chance of a $10-15 move higher. What could drive it?

- Middle East escalation: Any disruption to Strait of Hormuz transit — through which roughly 20% of global oil supply passes — could add $20-$40 to crude prices within days.

- OPEC+ production cuts: An emergency production curtailment, though unlikely given current pricing, would tighten an already nervous market.

- Sanctions enforcement: Stricter enforcement or expansion of sanctions on major producers could pull supply offline faster than the market expects.

- Inventory draws: If upcoming EIA weekly reports show continued draws against expectations, the cumulative effect could steepen the backwardation curve.

Conversely, a ceasefire, demand collapse, or strategic petroleum reserve release could push oil back toward $80-$90, activating the downside strikes.

What the Strip Is Really Saying

Pull the lens back and this market tells a coherent story: crude oil is already elevated (above $95 with high confidence), traders expect further upside with a median around $115-$120, and an unusually large share of capital is positioned for a genuine supply crisis that sends prices above $150. The downside is discounted but not dismissed — the 17.5% probability on the ↓$80 strike shows the market hasn't fully committed to the bull case.

The volume inversion — tail strikes trading more actively than at-the-money strikes — is the most important structural signal. In traditional options markets, this pattern (high demand for deep out-of-the-money calls) signals hedging activity, not speculation. Someone with physical exposure to oil prices — an airline, a refiner, a sovereign wealth fund — might use these Polymarket contracts as a cheap hedge against catastrophic price moves. The $200 strike at 3.9 cents is cheaper than most OTC options with similar characteristics.

Alternatively, this is pure speculative flow — crypto-native traders treating oil price contracts like meme coins, buying lottery tickets on geopolitical chaos. The data doesn't let us distinguish between these motives, but the practical effect is the same: the market is pricing fat tails, and it's doing so with conviction.

Traders tracking these strikes in real time can follow the full probability curve on FrenFlow, where each contract's price movement maps directly to shifting market expectations about the geopolitical and supply landscape.

With 12 settlement prints remaining and $1.51M in liquidity spread across 25 strikes, this market will be violently sensitive to headlines. A single CME settlement above $120 resolves half the strip. A single settlement below $75 flips the other half. The market has priced in uncertainty — but the skew tells you which direction the fear is pointing.

Frequently Asked Questions

What is the current oil price implied by Polymarket's crude oil market?

The strip prices imply that WTI crude oil's CME front-month settlement is currently in the $105-$110 range. The ↑$100 strike trades at 90.5% (near-certainty), while the ↑$110 strike sits at 73.5%, and ↑$105 at 84.7%. These probabilities are consistent with a current settlement price around $105-$108.

What are the odds of oil hitting $150 on Polymarket?

As of March 14, 2026, the ↑$150 contract trades at 16.4 cents, implying a 16.4% probability that WTI crude oil's CME settlement price reaches $150 or above on at least one trading day before March 31, 2026. This contract has attracted $4.35M in volume — among the highest in the entire strip.

Could oil reach $200 a barrel by end of March 2026?

Polymarket prices this at 3.9%, with $4.67M in total volume — the single highest-volume strike in the market. Historically, crude oil has never doubled within a single month. This contract functions more as a tail-risk hedge or speculative lottery ticket than a consensus forecast. A $200 settlement would require an unprecedented supply disruption.

How does this Polymarket oil contract resolve?

Resolution is based solely on the official CME daily settlement price for the active (front-month) crude oil futures contract. Intraday spikes, overnight Globex prices, and unofficial quotes do not count. If the settlement price meets or exceeds a given strike on any trading day through March 31, the corresponding "hit" contract resolves Yes.

Why is there so much volume on extreme oil price strikes on Polymarket?

The inverted volume pattern — more trading on $150-$200 strikes than on near-the-money $105-$110 strikes — suggests a combination of tail-risk hedging and speculative lottery-ticket buying. At 3.9 to 16.4 cents, these contracts offer 6x to 25x payouts, attracting risk-seeking capital. The pattern mirrors deep out-of-the-money call option demand in traditional markets during periods of geopolitical tension.